On this page

Subscription video on demand services (SVODs) must meet their expenditure obligations under the Broadcasting Services Act 1992 by spending money on eligible Australian programs. In each reporting year, an SVOD must acquit:

- its Australian content expenditure requirement for that year (if any amount of the expenditure requirement is not acquitted in the year it has been incurred, it can be acquitted in the 2 following reporting years)

- any shortfall Australian content expenditure requirements carried over from previous reporting years.

SVODs acquit their expenditure requirement by reducing it (but not below zero) by:

- the service’s qualifying expenditure amount (if any) for the reporting year

- any carried forward expenditure amount the service has from the previous one or 2 reporting years.

How the acquittal cycle works

The Act allows SVODs to carry forward excess qualified expenditure (referred to as carry-forward) and outstanding expenditure requirements (referred to as shortfall) across a 3-year acquittal cycle.

Put another way, following a reporting year, an SVOD has 2 additional years to make up any shortfall for that year (before being non-compliant with the Act). Alternatively, it can use up any carry-forward for that year (before it expires).

This is intended to account for the nature of production cycles, where expenditure across multiple years may vary.

The 3-year acquittal cycle is explained in section 121FZI of the Act. Key concepts in the acquittal cycle are that SVODs:

- must acquit shortfalls in chronological order

- must use carry-forwards in chronological order

- must carry forward any shortfall, even if the shortfall is overdue (that is, it is more than 2 years old) and the Act has been contravened

- cannot hold on to carry-forward (in whole or part) more than 2 years after the year it was incurred

- must continue to acquit any shortfalls even if the service no longer meets the definition of a regulated SVOD.

- SVODs contravene the Act if at the end of a reporting year they have a shortfall that has not been acquitted for 2 or more reporting years prior to the current year.

An SVOD can elect to use the revenue method to meet its requirements for a period of 3 years. It cannot elect to use this method if it has overdue shortfall.

Examples of the acquittal cycle

Different scenario examples are provided in the figures below to demonstrate the key concepts of the acquittal cycle. In these examples:

-

an SVOD’s total program expenditure, expenditure requirement and revenue are kept mostly consistent in each example for the purposes of simplicity.

- Qualifying expenditure (QE) means the amount of expenditure incurred by an SVOD in the reporting year on eligible Australian programs before they were made available to the public in Australia (on any service or location other than cinema).

- Total program expenditure (TPE) means expenditure incurred in the reporting year on eligible programs (drama, children’s, documentary, arts and education programs) that are, or are intended to be, provided on the service in Australia.

- Regulated SVOD has the meaning set out on this page.

- Requirement means the SVOD’s Australian content expenditure requirement – that is, the amount they must spend on eligible Australian programs in the reporting year – calculated based on its nominated acquittal method.

- Revenue means revenue derived by the Australian service each SVOD reporting year. Find out more.

- Carry-forward means a carried forward qualifying expenditure amount.

- Shortfall means outstanding expenditure requirement for each SVOD reporting year.

- Year means the relevant SVOD reporting year beginning 1 January and ending 31 December.

Find out more about TPE and QE.

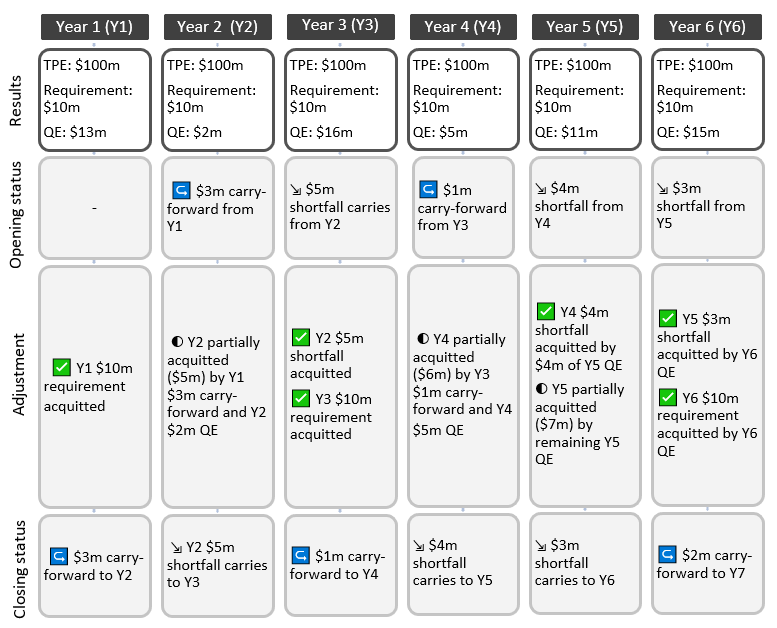

Figure 1: Qualifying expenditure fluctuates from year-to-year

SVOD A acquits its requirement using the expenditure method. While its total program expenditure remains stable for its Australian service, it concentrates significant investment in a small number of eligible Australian programs, resulting in fluctuations in its qualifying expenditure. Each year’s requirement is acquitted within the required 3-year cycle.

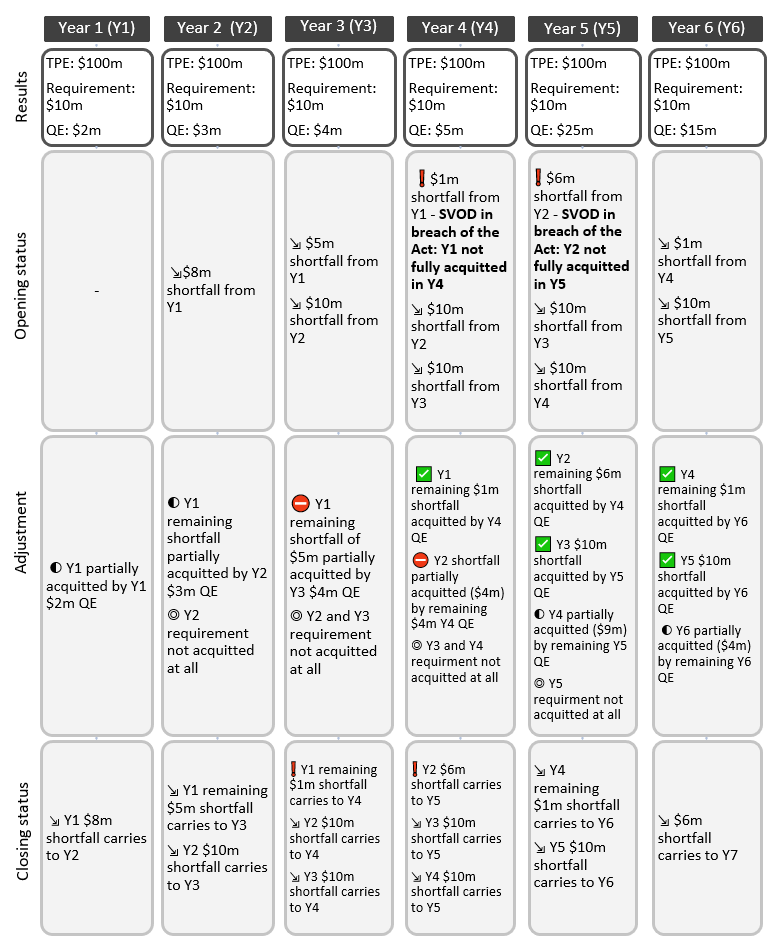

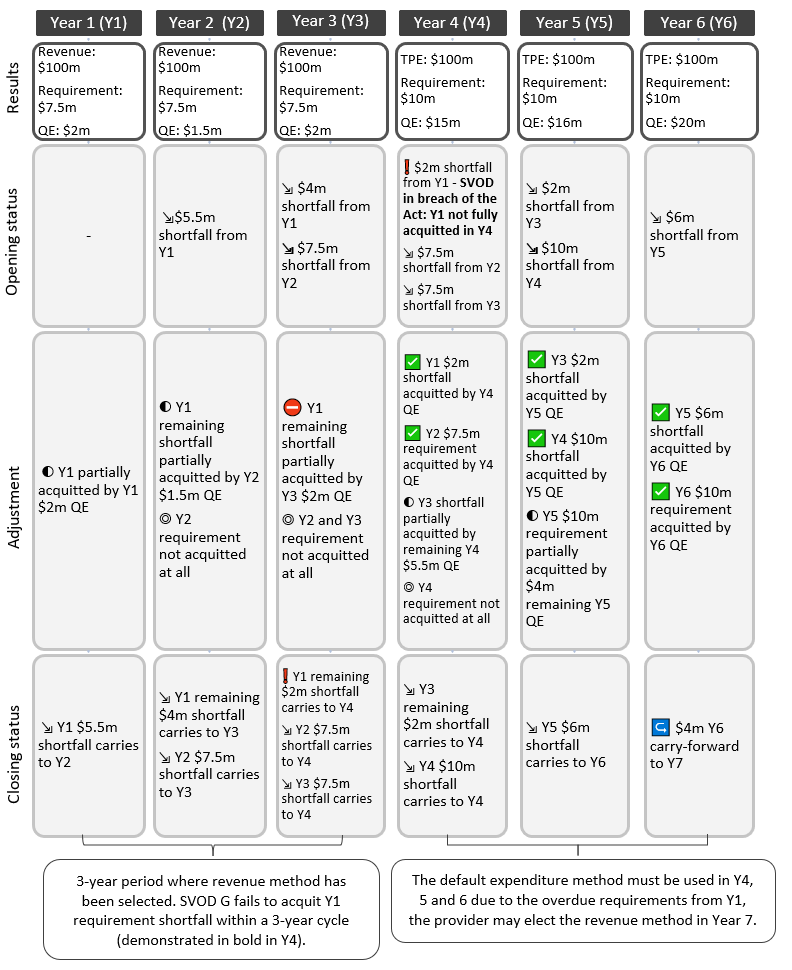

Figure 2: Ongoing failure of the SVOD service to meet its requirement

SVOD B acquits its requirement using the expenditure method. Because it consistently spends less on eligible Australian programs than required, it fails to fully acquit its year one and year 2 requirements within their 3‑year periods and contravenes the Act.

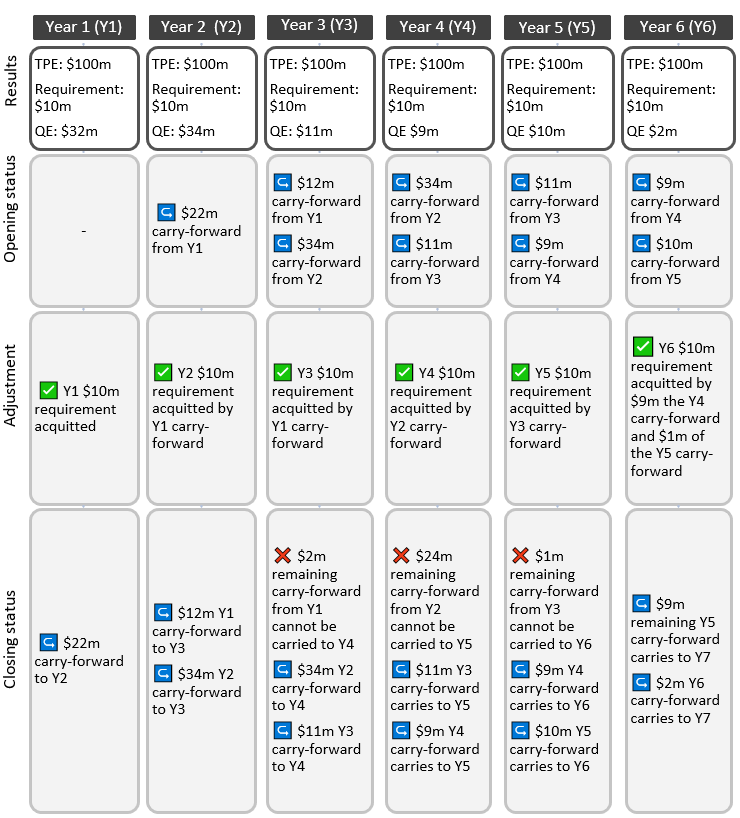

Figure 3: Qualifying expenditure consistently exceeds requirement

SVOD C acquits its requirement using the expenditure method. It consistently spends more on eligible Australian programs than required. In year one, SVOD C spends enough money to carry the excess expenditure forward and use it to meet its requirements in years 2 and 3. Carry forward can only be used for 2 years after its expenditure year, so in this example, it cannot be used from year 4 onwards. The same rules apply to the carry forward generated in years 2 and 3.

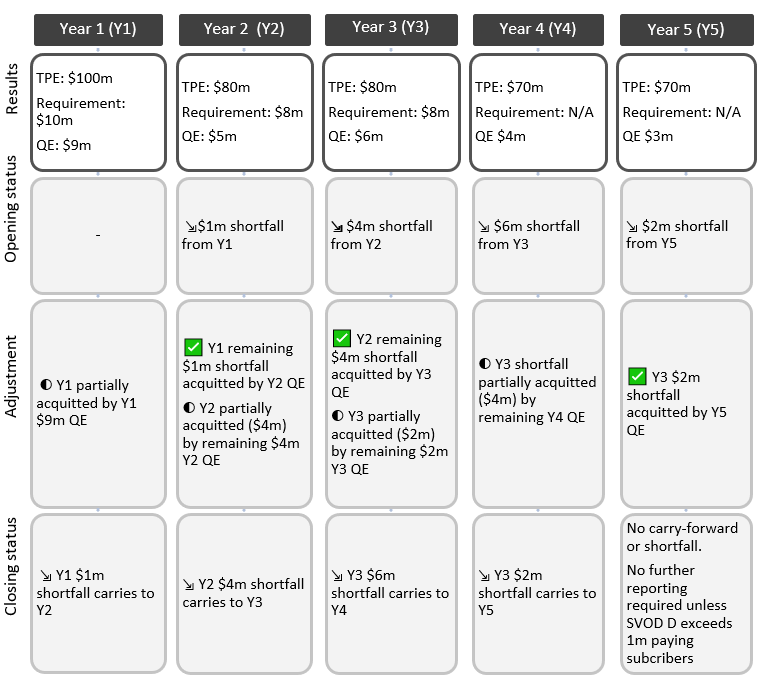

Figure 4: The subscribers to the provider’s SVOD service drop below one million

SVOD D is a regulated SVOD in years one, 2 and 3. Part of the way through year 3, it drops below one million paying subscribers and is no longer a major SVOD from year 4 onwards. Even so, SVOD D must continue to report to the ACMA until it acquits its outstanding requirement.

Figure 5: The SVOD service wholly acquits its expenditure requirement each year

SVOD E consistently acquits its Australian content expenditure requirement each year, with no expenditure shortfall and no qualifying expenditure carried over between reporting years.

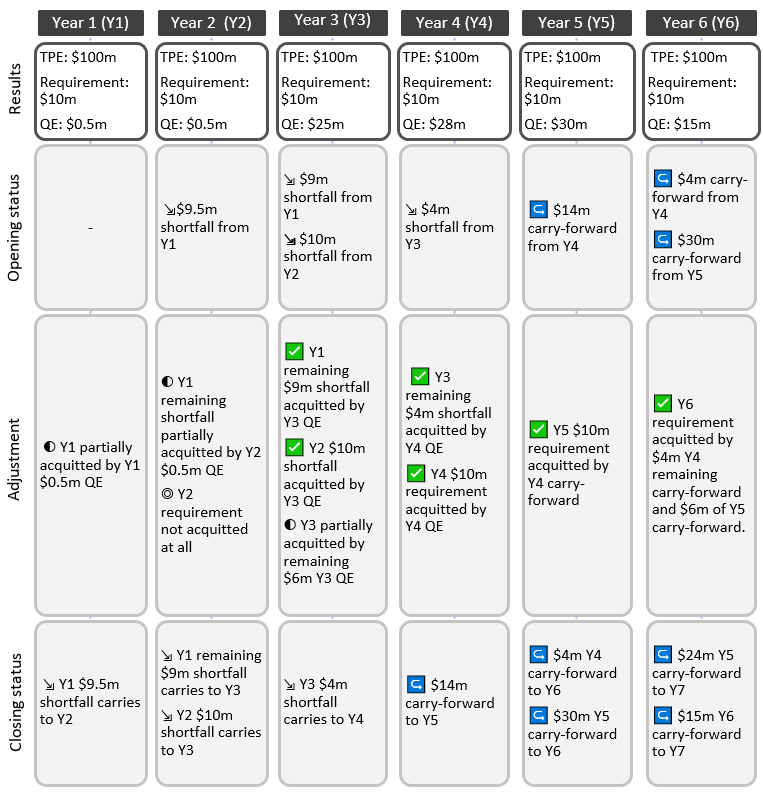

Figure 6: Expenditure shortfalls are acquitted within the 3-year period

SVOD F’s qualifying expenditure is well below its requirement in years one and 2. From year 3, it increases its investment in eligible Australian programs. This allows it to meet its outstanding requirements and to carry‑forward expenditure.

Figure 7: Service provider selected the revenue acquittal method, however, cannot re-elect this method after the 3-year period

SVOD G elects the revenue method in year one. At the end of the 3-year period, it has an overdue shortfall requirement for year one and must default to the expenditure method for the next 3-year period. The overdue shortfall is made up, and it may elect the revenue method again in year 7.

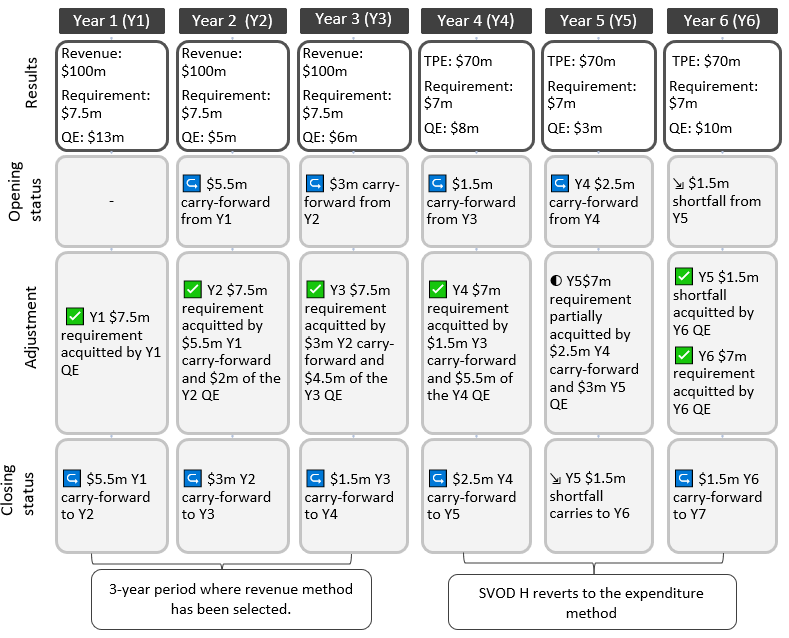

Figure 8: Service provider selected the revenue method then reverts to the default expenditure method after the 3-year period

SVOD H elects the revenue method in year one. At the end of a 3-year period, it has acquitted the requirement for all 3 years, however, chooses not to re-elect the revenue method. Instead, SVOD H reverts to the default expenditure method.

More information

If you have any questions, please email svodauscontent@acma.gov.au.

- This information is accurate as of May 2026.

- It may be updated as content requirements are implemented.

- This is not legal advice.

- SVODs should seek their own advice about their obligations under the Broadcasting Services Act.

- The term ‘SVOD’ refers to providers of subscription video on demand services.